The Russian invasion of Ukraine enters 2024 with significant uncertainty and high stakes. Russia and Ukraine view 2024 as a waypoint in what is almost certainly a long war marked by intense attrition, limited territorial change, and perceived medium to long-term opportunities to achieve their maximalist objectives. Our Look-Ahead provides an outlook of the war in 2024, based on the following points: War aims for 2024 and beyond; strategy & tactics; force (and) attrition); ammo & fires, defense industry; defense spending & state budget; external support; and other considerations (power grid, shipping, negotiations).

KEY JUDGEMENTS

- The Russian invasion of Ukraine will very likely persist as a high-intensity attritional and positional war in 2024. Ukraine is in danger of losing more territory than in 2023 and is virtually certain to adopt a strategic defense posture and rebuild reserves for most of the year, in preparation for a perceived better 2025. Russia is likely to continue meatgrinder-type offensives, as seen in Bakhmut, Vuhledar, and Avdiivka in 2023.

- Ukraine and Russia are most likely to retain their maximalist war aims in 2024– Ukraine: return to 1991 borders; Russia: full political-military control of Ukraine. Kyiv likely perceives 2024 as a detour, but not abandonment, of its final war aim. Moscow likely sees next year as a waypoint to victory in the 2025-2027 timeframe. Complete conquest of the Donbas and Oskil River Valley (Kharkiv oblast) is Russia’s likely operational objectives for 2024, although those are unlikely to be met.

- Ukraine and Russia will continue to ramp up defense industry output in 2024. Ukraine will focus on drones, especially FPV and one-way attack drones (OWAD), project FrankenSAM with the U.S., vehicle production, missiles, and a variety of other programs with Western partners. Russia will also focus on drones, FPV, OWADs and others, vehicles, loitering munitions, glide bomb kits, missiles, and other systems. In terms of defense spending, Russia’s will increase by 30% (total $140 billion) while Ukraine’s will decrease slightly from 2022 (total $44 billion).

- Ukraine will likely experience a decline in U.S. and European military and financial aid in 2024 due to cabinet changes, upcoming U.S. elections, and so-called “war fatigue.” Russia will continue efforts to rally support in the “Global South” for its war in Ukraine, foment anti-Western sentiment, and encourage regional conflicts elsewhere. External support is one of the most decisive variable in how the war will evolve in 2024.

- The prospects of a negotiated armistice between Ukraine and Russia remain low in 2024, although higher than in 2023. Backchannels via Saudi Arabia, the UAE, Turkiye, and other intermediaries are likely to remain open should opportunities arise.

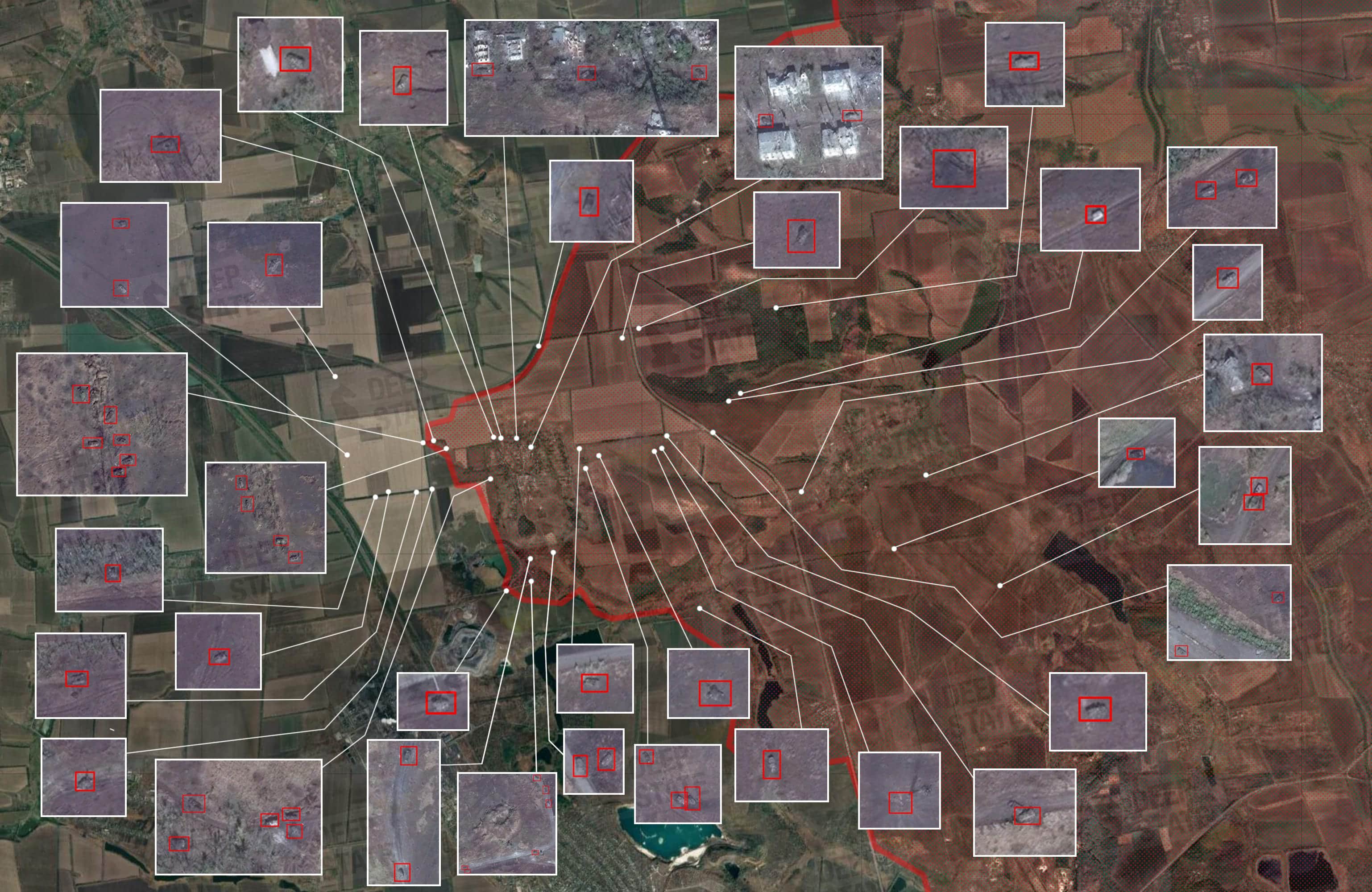

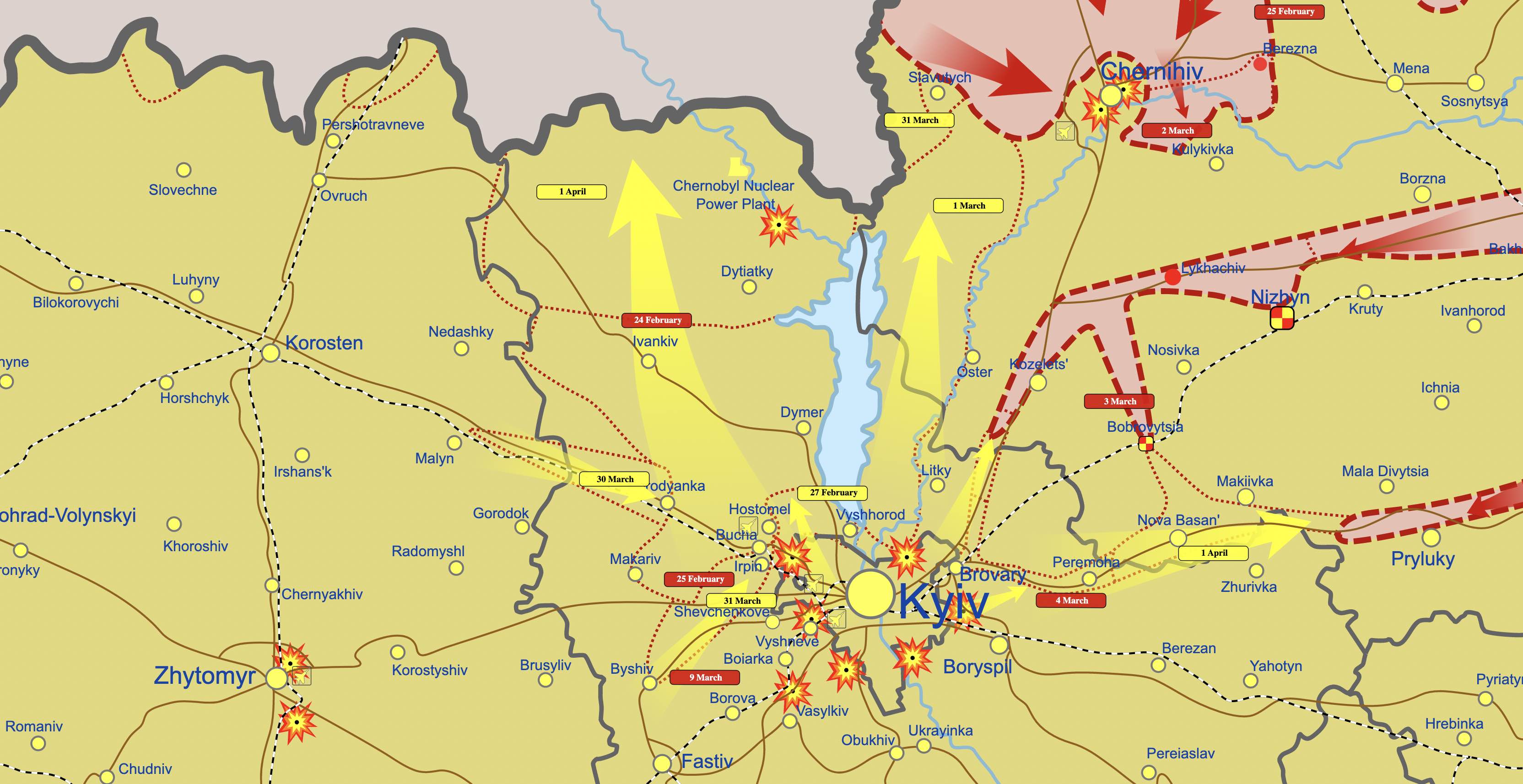

Territorial control in Ukraine as of 3JAN24 (©DeepStateUA)– green: territory reclaimed by Ukraine since 24FEB22; purple: Russian-occupied territory since 2014; red: territory occupied by Russia since 24FEB22 (except “Transnistria” in Moldova)

WAR AIMS IN 2024 AND BEYOND

RUSSIA: OLD GOALS, NEW CONFIDENCE

2024 Outlook

Russia’s primary focus in 2024 will likely remain the full conquest of the Donbas -Donetsk and Luhansk oblasts- coupled with securing control over the Oskil River valley in Kharkiv oblast.

The strategic objective of gaining military control over the four annexed regions (4ARs) – Donetsk (57% occupied), Luhansk (98%), Kherson (72%), and Zaporizhia (72%) – will also remain a top priority.

Completing the occupation of the Donbas and/or the 4ARs within 2024 is highly unlikely.

Beyond 2024

President Vladimir Putin likely sees 2024 as a waypoint to achieving complete victory in the later half of this decade, with 2025-2027 as his envisioned culmination period.

Putin has not abandoned his maximalist goals of complete territorial and political control in Ukraine. His DEC23 public statements indicate a newfound confidence that Russia will prevail in the long term.

Putin’s theory of victory hinges on the belief that Russia will outlast both Western support for Ukraine and Ukrainian manpower and industrial ability to continue the war.

Putin’s long-term goals are unlikely to be achieved in the current conditions of Q4 2023. Ukraine’s determination to resist remains unwavering, and its military capabilities, both defensively and offensively, have significantly and irreversibly strengthened, with continuous growth. Meanwhile, Russia failed to transform its numerical superiority into a clear offensive advantage.

UKRAINE: DETOUR AHEAD

2024 Outlook

Ukraine is likely to focus on limiting territorial losses in 2024, as it prepares for a year of declining foreign aid and continued attrition. Possible counteroffensives may occur, but these will likely be more localized and limited in scope.

While 2024 may not be defined by major counteroffensive operations, Ukraine is likely to sustain, and even increase, long-range strikes against targets in occupied Crimea and Russia using homegrown weapons.

Territory change in 2023 (@Pouletvolant3/ yellow-Ukrainian liberation; blue- Russian occupation)

There is a major risk that Ukraine will lose more territory in 2024. The net surface loss could be more than in 2023 (nearly -0.05%), but less than in early 2022 (-17%). In 2023, Ukraine experienced a net territorial loss of 288 km2– it gained 395 km2 while losing 683 km2 (estimates vary).

Russia currently occupies around 17.48% of Ukrainian territory, including Crimea.

The 2024 outlook for Ukraine is fluid and hinges on addressing military recruitment challenges, securing further Western military and economic aid, boosting defense-industrial output, and Russia’s performance in upcoming offensive campaigns.

Beyond 2024

Ukraine’s assessed 2024 war aim can be seen as a detour but not an abandonment of its own maximalist objectives of returning to 1991 borders.

Kyiv is likely also counting on a more favorable post-2024 in terms of foreign support, although this is contingent on U.S. electoral results, willingness/ability of Europeans to step in, and combined Western-Ukrainian defense industrial output.

Ukraine’s long-term strategic goals are likely not aligned with most allied and partner states, many of which only intend to improve Ukraine’s ability to negotiate.

STRATEGY AND TACTICS

RUSSIA: MEATGRINDER OFFENSIVES

Russia is likely to continue meatgrinder-type offensives on all primary axes of attacks. This modus operandi will likely perpetuate the trend of incremental gains but high losses, as seen in Bakhmut, Vuhledar, and Avdiivka in 2023.

Russia lost 200 vehicles in just one week of the Avdiivka offensive in OCT23 (@UAControlMap)

Russian Chief of General Staff and Commander of Russian forces in Ukraine, General Valery Gerasimov, favors a perpetual offensive posture, driven by political and doctrinal motivations. This is evident by his major offensives from early Winter, late Summer (north Luhansk), and late Winter 2023, along with the constant small offensive actions across the entire 1,000-km active frontline throughout the year.

Key focus points:

- Luhansk (and Kharkiv):

- recapture or contest Kupyansk.

- recapture the left bank of the Oskil river valley (Kreminna-Svatove line)

- Donetsk:

- return to the Lyman-Yampil salient.

- reach the Konstantynivka-Kramatorsk-Slovyansk (K2S) urban belt.

- capture the Avdiivka sector

- Zaporizhzhia:

- rollback Robotyne balcony

- Kherson:

- eliminate Ukrainian bridgeheads on the left bank of the Dnipro.

- Crimea:

- enhance the south Ukraine “land bridge” by expanding the coastal highway and building a new direct railway linking occupied Crimea with Mariupol.

- Black Sea:

- interdict commercial shipping to and from Ukraine, confront Ukrainian asymmetric warfare at sea, and deter NATO ISTAR activity.

UKRAINE: STRATEGIC DEFENSE

Ukraine is likely to adopt a strategic defense posture in 2024. Ukraine is compelled to adopt a defensive posture due to the expected decline in U.S. military aid and the requirement to regenerate forces after the months-long CO.

While spending most of 2024 on defense with limited counteroffensive opportunities, Ukraine has the chance to, and must, rebuild reserves, refine tactics, and expand its forces. The potential for a return on the offense in Q4 2024 or 2025 exists if external and domestic factors are favorable.

Ukrainian forces are actively fortifying and reinforcing defensive lines to better withstand ongoing and upcoming Russian assaults. This defensive strategy involves the installation of dragon’s teeth obstacles, fortifying trenches, and creating or expanding minefields. This will create similar physical dilemmas for Russian offensives as the “Surovikin line” posed for Ukraine’s counteroffensive in Zaporizhzhia. However, due to potential constraints in ammunition and manpower availability, Ukraine may face difficult decisions regarding which sectors to defend in front of Russian meatgrinder assaults.

Compilation of various UA MOD images and videos of frontline engineering work

Key focus points:

- Luhansk (and Kharkiv):

- defend Kupyansk

- halt/roll back Russian advance on the Oskil River Valley.

- Donetsk:

- hold the line in Yampil-Lyman

- contain Russian advance in the Bakhmut sector (defend Chasiv Yar; prevent a return to Siversk; keep the K2S line out of artillery range).

- inflict maximum losses on the enemy while fighting a delaying action in Avdiivka.

- Hold the line in the broader southwestern Donetsk.

- Zaporizhzhia:

- hold and improve positions.

- eye the expansion of the Robotyne balcony as an action of opportunity.

- Kherson:

- Expand and/or increase bridgeheads on the left bank of Dnipro;

- eye a breakthrough as an action of opportunity.

- Crimea:

- continue missile attack campaign against Russian occupation and Black Sea Fleet.

- target and destroy the Kerch Bridge.

- Black Sea:

- protect the commercial shipping corridor.

- deny the northwestern sector and the Odesa-Bosphorus/Odesa-Danube shipping lanes to Russia.

FORCE (AND) ATTRITION

RUSSIA: COLOSSAL LOSSES

Casualties

Russia is likely to continue suffering substantial human losses in 2024, with a cumulative total expected to reach 400,000 to 500,000 killed in action (KIA) and wounded in action (WIA) since the full-scale invasion began on 24FEB22.

Russia’s current total casualty estimate stands at 315,000– an estimated 87% of the pre-war armed forces (DEC23 assessment).

In 2023, Russia lost around 215,000 forces. Russia reached its highest troop and equipment loss in Q4 2023 in the Avdiivka offensive, followed by Q3 2023 with the Ukraine Summer Counteroffensive.

This marks an approximate 100% attrition increase from 2022 when Russia suffered “over 100,000 casualties.”

If Ukraine continues to impose such a casualty rate, the Russians will be unlikely to mount a significant offensive and seize major objectives. A loss rate of at least 50,000 casualties/6 months would be enough to blunt Russia’s force regeneration and offensive potential, according to Estonian Intelligence.

Fighting force

Despite the heavy losses, Russia marshalls 420,000 forces in Ukraine (SEP2023 Ukrainian estimate). This is thanks to a mix of stop-loss measures, informal recruitment pipelines, and a partial mobilization in late 2022, which has not fully concluded.

Tens of thousands of additional forces are very likely still contributed by the 1st and 2nd Corps (so-called “Donetsk and Luhansk People’s Republics”) and the Russian National Guard.

Long-term plans call for surging Russian Armed Forces even further. On 1DEC, Putin signed a decree to increase the maximum number of servicemen by 170,000- a 15% increase from the current cap of 1,320,000.

The Russian Defense Ministry aims to increase the number of contract servicemen in the Russian Armed Forces to 745,000 by the end of 2024.

Vehicles

Russia is anticipated to sustain a high attrition rate in vehicles and military equipment in 2024. Although its defense industry is expected to continue replacing destroyed vehicles, including tanks, the overall quality of the vehicle fleet is likely to decline as refurbished vehicles pulled from storage become increasingly older– and some unrepairable.

In 2023, Russia lost 4,978 vehicles. This is 41.87% less than in 2022 (8,560).

Russian tank losses in 2023 are at 971, around 39.31% less than in 2022 (1,600).

Russia lost a total of 13,538 vehicles, including 2,571 tanks, since 24FEB22.

Note: data courtesy of Oryx Blog (timeframes compared 1JAN23 vs. 20DEC23)

UKRAINE: ECONOMY OF FORCE

Casualties & Fighting Forces

Ukraine likely has around 40-50% fewer casualties than Russia, although there are no recent and reliable estimates of Ukrainian manpower losses. This trend is likely to hold steady in 2024 but could worsen depending on ammunition availability and how the war develops.

Ukraine has around one million people under arms. However, this total includes non-frontline forces, such as administrative and internal security units in the rear, reserves, and border personnel spread out along Ukraine’s 2,500-km border with Russia. The number of frontline troops is most likely significantly lower.

Ukraine requires further mobilization and improvement of current incorporation measures to sustain or surge its manpower in 2024. The Ukrainian General Staff wants to mobilize 450,000-500,000 people next year- a decision that is yet to be approved by Ukrainian President Zelensky.

Vehicles

Ukraine will likely aim to preserve big-ticket items and reduce equipment losses in light of declining foreign military aid in 2024.

Ukraine lost 2,159 vehicles in 2023. This is 19.31% less than in 2022 (2,677 vehicles).

Ukrainian tank losses in 2023 are at 271, around 37% less than in 2022 (430).

Ukraine lost a total of 4,836 vehicles, including 701 tanks, since 24FEB22.

In contrast, Russia has 179.96% more visually confirmed vehicle losses than Ukraine.

Note: data courtesy of Oryx blog (timeframes compared 1JAN23 vs. 20DEC23)

AMMO & FIRES

RUSSIA: NUMERICAL SUPERIORITY

Russia is expected to maintain numerical superiority but face qualitative inferiority in artillery ammunition, particularly in 152mm and 122mm, compared to Ukraine. Russia is likely seeking more avenues to bolster artillery ammunition, such as importing and scaling up its own production.

Russia is entering 2024 with an estimated four million artillery shells in reserve. In addition, Russia received 350,000 shells from North Korea/DPRK in Q4 2023. However, North Korean shells are of mixed quality, and a significant share has already been consumed.

UKRAINE: SHELL HUNGER

Ukraine is likely to experience numerical inferiority but maintain qualitative superiority in artillery ammunition compared to Russia. Despite the quality edge, Ukraine can offset Russian artillery advantages through superior counter-battery fire, MLRS, and precision-guided fires, although the effectiveness of the latter is impacted by the widespread use of Russian tactical electronic warfare (EW) systems.

In addition, the qualitative advantage may erode as ammunition diminishes for Ukraine’s superior Western-made artillery systems.

Ukraine is entering 2024 with whatever it has left from the over one million artillery shells received from U.S. strategic stocks for the Summer Counteroffensive (CO). The leftover inventory is expected to be low due to the high expenditure during active operations, reaching up to 10,000 shells per day. Ukraine is already experiencing shell hunger and has to curtail operations in some areas on the front.

155mm shells produced by Rheinmetall (©Rheinmetall)

Ukraine is unlikely to receive the one million artillery shells promised by the European Union by Q2 2024. Only 300,000 shells have been delivered so far in Q4 2023. Ukraine must pursue alternative avenues to replenish and supplement artillery ammunition. Domestic 155mm shell production is expected to begin only in 2025.

DEFENSE INDUSTRY

The Ukrainian and Russian defense industries cannot be directly compared due to systemic differences in size, production capacity, and their roles in supplying their respective armed forces. This section examines the outlook, strategies, and major programs in progress related to production and refurbishment.

RUSSIA: SHIFT TO WAR GEAR

The Russian defense industry is poised to continue to intensify production in crucial areas during 2024. This includes artillery ammunition (e.g. Krasnopol, 152mm), tanks (T-90M, T-80BVM), armored vehicles (BMP-3), loitering munitions (Lancet-3, Scalpel), drones (including FPV), and glide bomb kits in 2024. Putin specifically ordered Rostec CEO Sergey Chemezov to increase the production of Lancets and FPV drones.

Uralvagonzavod (UVZ) will continue to reactivate old tanks from storage, such as T-62, T-64, and T-55, for attritional use in Ukraine. UVZ’s tank output likely ranged from 1,000 to 2,000 units in 2023, with new production batches being a minority (around 200/year).

T-90M and T-72B2 assembly lines at UVZ

JSC SEZ PPT Alabuga is likely to produce between 100 and 200 localized Shaheds 136 (Geran-2) per month in 2024. Alabuga’s current production rate is over 100 Shaheds/month, and it aims to achieve 226/month by September 2025.

Russia is expected to experience a moderate upturn in long-range missile production in 2024. Based on Ukrainian Military Intelligence estimates, Russian missile manufacturers have already managed to increase output in 2023:

- Kh-101: 35 (MAY23) -> 40/month (AUG23)

- Kalibr (outlier/decrease): 25/month (MAY23) -> 20/month (AUG23)

- Kinzhal: 5/month (MAY23) -> ?/month (AUG23)

- Iskander-M: 5/month (MAY23) -> 30/month (AUG23)

- Iskander-K: ?/month (MAY23) -> 12/month (AUG23)

- Kh-32: ?/month (MAY23) -> 10/month (AUG23)

UKRAINE: RISING FROM ASHES

The Ukrainian defense industry is poised to start and increase production in crucial areas during 2024. This includes long-range one-way attack drones/OWADs (UJ-22, UJ-26 Beaver, Scythe 400), FPV drones, strategic missile systems (Neptune, Long Neptune, Hrim-2), unmanned surface vessels (Magura, Sea Baby, Mamay), and maintenance, repair, and overhaul (MRO) capabilities.

View from a Ukrainian FPV drone attacking a Russian tank (social media footage screenshot)

Another major priority for 2024 is to strengthen cooperation with Western defense industries to localize and transfer technology and production to Ukraine. Ukraine signed dozens of joint production and technology transfer agreements with Western defense companies in Q3/Q4 2023.

Key projects, expected to yield results in 2024, include:

- Project FrankenSAM: joint Ukraine-U.S. initiative to reactivate Ukraine’s Soviet-era air defenses by arming them with Western RIM-7 SeaSpearrows.

- UAVs, especially FPV drones: 1,000,000 expected output in 2024 (FPV drones are also sought as a way to offset/not replace artillery shortage).

- Multiple OWADs: serial production expected to yield high UJ-26 Beaver and Scythe 400 numbers; key to imposing a retaliation dynamic for Russian air campaigns, and hitting Russian targets and infrastructure in the rear.

- Rheinmetall UDI: Rheinmetall-Ukroboronprom joint venture to produce Fuchs and Lynx vehicles, and set up local MRO, in Ukraine.

- Long Neptune: extended-range Neptune.

- Hrim-2: missile improvement.

- Bohdana self-propelled artillery: increase production to over 6/month.

DEFENSE SPENDING & STATE BUDGET

RUSSIA: $140 BILLION

Russia is estimated to spend $140 billion (12,765 billion roubles) on defense in 2024, or roughly 7.1% of GDP. Defense spending will take around 35% of the 2024 state budget and represent a 30% surge from the previous year. However, actual war-related expenses are likely to surpass these figures, encompassing sectors beyond traditional defense.

The Russian economy is forecasted to grow by 1.1% in 2024, slower than previously forecasted by the International Monetary Fund (IMF). In 2023, the economy saw a 2.2% growth.

The slow rate of Russian economic contraction, coupled with a historic surge in defense spending, suggests Moscow’s readiness and financial capacity for a long war with Ukraine, and unparalleled militarization.

UKRAINE: $44 BILLION

Ukraine is estimated to spend $44 billion (1,692 billion hryvnias) on defense in 2024, or roughly 22.1% of GDP. This amounts to 50.54% of the 2024 state budget. This is less than Ukraine spent on defense in 2023 (37-39% of GDP) and 2022 (30.8%), according to Wilson Center estimates.

Ukraine’s 2024 defense spending may end up being higher than originally indicated, as seen in previous years.

The Ukrainian economy is forecasted to grow by 3.2% in 2024. This marks a marginal increase from the 2% growth assessed in 2023.

EXTERNAL SUPPORT

RUSSIA: FRIENDS IN HIGH PLACES PRODUCTION

Russia is virtually certain to continue receiving political and military-industrial support from allied authoritarian regimes in 2024. Russia will continue efforts to rally support in the so-called “Global South” for its war in Ukraine, foment anti-Western sentiment, and encourage regional conflicts elsewhere (e.g. Guyana, Red Sea, East Asia).

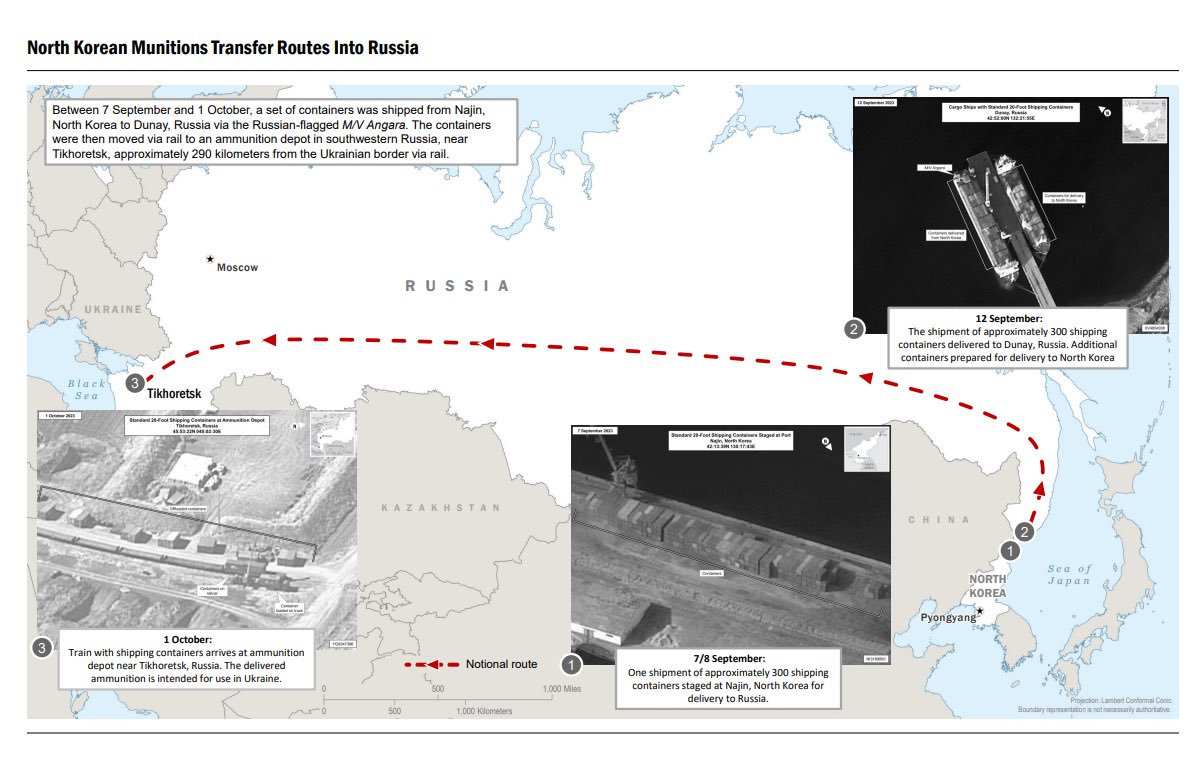

North Korean Munitions Transfer Routes into Russia (© U.S. Department of Defense)

- North Korea: High risk of follow-on 122mm and 152mm ammo deliveries and transfer of MLRS and missile systems, such as KN-23.

- Iran: Risk of ballistic missile transfers given official completion of Su-35 deal. There is likely also an open-door policy for providing other missiles and drones, including jet-powered Shaheds, if Russia reciprocates. Iran is expected to remain Russia’s foremost ally in its aggression against Ukraine.

- China: Risk of Chinese under-the-radar support in ramping up Russian industrial output, such as in bomb-laden FPV drones and tactical equipment manufacturing and exports in transport, logistics, and engineering equipment. Beijing is also likely to increase export controls to ensure it is not inadvertently aiding Ukraine’s FPV drone production.

UKRAINE: DECLINING SUPPORT

Ukraine will likely experience a decline in military and financial aid from the U.S. and EU in 2024 due to recent cabinet changes in some European capitals and upcoming U.S. elections. This is likely the single most decisive variable in how Ukraine will perform on the battlefield in 2024.

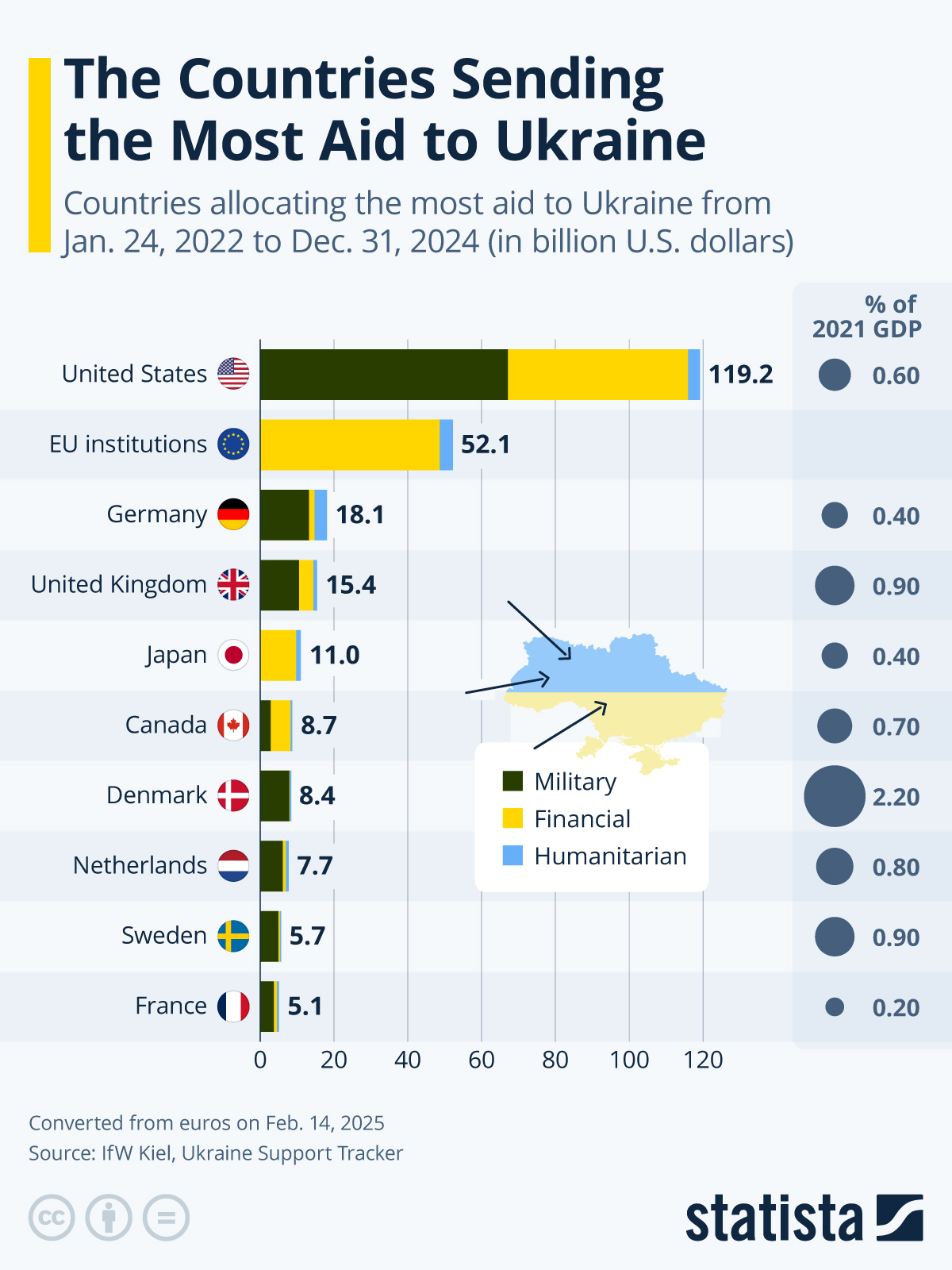

The countries committing most aid to Ukraine (©Statista)

Ukraine will most likely not be abandoned politically, nor will financial and military supplies cease completely. This is a near certainty as Ukraine has multi-year commitments from top EU contributors and joint production agreements.

- U.S: severe risk looms over the reduction or cessation of economic and material military aid in 2024. Without U.S. aid, Ukraine’s ability to launch new counteroffensives and defend its entire frontline territory diminishes, potentially resulting in substantial territorial and human losses, lowered popular morale, and constrained political options in prosecuting the war.

- EU states: European countries are expected to step up leadership in 2024. However, political, economic, and military limitations may hinder them from fully replacing U.S. contributions, particularly in terms of military aid.

- Germany: Expected to remain the leading non-U.S. financial donor to Ukraine in 2024. Berlin’s newfound military support for Kyiv is also expected to continue, especially on the financial and industrial level.

- Netherlands: A Wilders-led government would introduce uncertainty in Dutch military support. While aid may not cease completely due to coalition and parliamentary dynamics, the stakes are high.

- Central and Eastern European (CEE) states: The Baltics are projected to maintain stability as allies, with Poland potentially returning as a regional leader, though support levels could dip. Hungary is likely to maintain pro-Russian stances, and Slovakia may follow a similar path. Romania is expected to remain a stable ally, though elections in 2024 could see the support scrutinized by nationalist opposition parties.

- UK: London is very likely to maintain its support for Ukraine in 2024. However, the prospect of general elections by Q1 2025 introduces uncertainty, especially from a non-Torry cabinet.

- East Asian allies: The robust output of Japan and South Korea could significantly impact Ukraine’s ammunition stocks and weapons capability. While direct transfers are moderately unlikely due to legislation, these allies might continue supporting Ukraine through third-party backfill donations.

OTHERS CONSIDERATIONS

UKRAINE: POWER GRID

Ukraine has stabilized its power grid but is bracing for a renewed Russian strategic bombing campaign over the 2023/2024 winter. Current reparation rates are (AUG2023):

- 100% high-voltage substations have been restored to pre-war levels.

- 80% Ukrenergo main power network.

- 70% of thermal power plants.

- 68% of hydropower plants.

- 62% of coal handling plants.

- 60% of nuclear power plants.

The percentages have likely improved further into Q4 2023.

Other developments that bolster Ukraine’s power grid security:

- Increased Western air defense presence in Ukrainian cities and critical national infrastructure (CNI) since 2022

- Project FrankenSAM reactivate Soviet-era air defenses that went offline in mid-2023 due to lack of ammo.

- Influx of foreign investments in Ukraine’s energy sector reconstruction, emphasizing renewables.

- British Army training for Ukrainian engineers to harden infrastructure and quickly repair damage caused by a variety of munitions.

- Ukraine expanded allowed electricity import volumes from the EU. Note that the Ukrainian power grid is connected to the ENTSO-E.

Note: T-Intelligence has extensively monitored Russia’s campaign against Ukraine’s power grid during the winter of 2022/2023 and will issue a report on the lessons learned in 2024.

UKRAINE: SHIPPING AND GRAIN TRADE

With British and allied regional help, Ukraine will likely manage to keep the Black Sea Shipping Corridor (BSSC) open for most of 2024. Over 150 shipping vessels have used the BSSC since Ukraine established it in AUG23. This amounts to 7 million tons of cargo, including nearly 5 million tons of Ukrainian agricultural products. Shipping on the BSSC is made possible by a special mechanism for discounts on war risk insurance agreed by Ukraine and the UK.

Ukraine is expected to receive new warships from the UK and Norway in 2024 as part of the Maritime Capability Coalition, contributing to the BSSC security.

UKRAINE-RUSSIA: NEGOTIATIONS

The prospects of a negotiated armistice between Ukraine and Russia remain low in 2024, although higher than in 2023. Systemic distrust between Russia and Ukraine, the mutual belief that the war is preferable to an unfruitful agreement, and continued maximalist war aims make a “sit down” unlikely. In addition, Russia has indicated that it is not willing to negotiate anything other than Ukrainian surrender.

Backchannels via Saudi Arabia, the UAE, Turkiye, and other intermediaries are likely to remain open should opportunities arise.

Any negotiated settlement in which Russia is not defeated or strategically weakened will almost certainly lead to an intermission favorable to Russia to rearm, regroup, and relaunch a more violent follow-on war.

By Vlad Sutea

Information cutoff point: mostly 20DEC23 (exceptions apply).

Quantitative data points: Government intelligence estimates (U.S.,UK, Estonia, Poland, Ukraine), Oryx Blog, @WarMapper, Deep State, and others.

Founder of T-Intelligence. OSINT analyst & instructor, with experience in defense intelligence (private sector), armed conflicts, and geopolitical flashpoints.

-

Vlad Suteahttps://t-intell.com/author/admin/

-

Vlad Suteahttps://t-intell.com/author/admin/

-

Vlad Suteahttps://t-intell.com/author/admin/

-

Vlad Suteahttps://t-intell.com/author/admin/

![Evacuation “Shattered Glass”: The US/ Coalition Bases in Syria [Part 1]](https://t-intell.com/wp-content/uploads/2020/02/KLZJan.62018copy_optimized.png)

![Pride of Belarus: Baranovichi 61st Fighter Air Base [GEOINT]](https://t-intell.com/wp-content/uploads/2021/08/cover_article.jpg)

![Evacuation “Shattered Glass”: The US/ Coalition Bases in Syria [Part 2]](https://t-intell.com/wp-content/uploads/2020/02/TelSalman24.2.2018_optimized.png)

![This is How Iran Bombed Saudi Arabia [PRELIMINARY ASSESSMENT]](https://t-intell.com/wp-content/uploads/2019/09/map4cover-01-compressor.png)